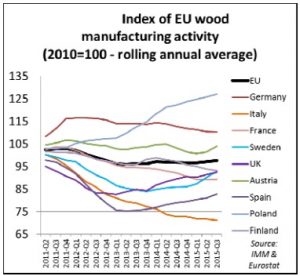

Demand for wood products has benefitted only a little from Europe’s slow economic recovery in the last three years. This is evident from the Eurostat index of EU wood manufacturing activity which covers the sawmilling, veneer, panels and joinery sectors but excludes wood furniture. European wood manufacturing activity remained stalled at around 97% of the 2010 level between the start of 2014 and second quarter of 2015.

Demand for wood products has benefitted only a little from Europe’s slow economic recovery in the last three years. This is evident from the Eurostat index of EU wood manufacturing activity which covers the sawmilling, veneer, panels and joinery sectors but excludes wood furniture. European wood manufacturing activity remained stalled at around 97% of the 2010 level between the start of 2014 and second quarter of 2015.

The stasis in European wood manufacturing activity is a reflection of the slow growth in the European construction sector. It also suggests that wood has yet to make significant inroads into market share of alternative materials.

Competition between suppliers of different wood products – such as between panels and sawn wood and between temperate and tropical hardwood - also remains intense.

While total European demand for wood products has remained flat, there are on-going significant shifts in the source of demand. Markets for sawn wood and woodbased panels have been particularly hard hit by the economic downturn and stagnation of the building and furniture sectors.

The wood veneer sector has suffered profoundly from the contraction of the southern European joinery manufacturing industry and has come under intense pressure from substitute materials and new finishing techniques across the European continent.

However new opportunities are arising for value-added engineered and other forms of modified wood products, particularly in structural applications. The combination of strong technical performance and reduced overall costs of construction are the main drivers for uptake of these modern wood products.

The carbon and sustainability message is a welcome bonus for those specifiers and contractors keen to burnish their green credentials. The relatively positive outcome of the recent Climate Change conference in Paris gives some confidence that this latter issue may become a more prominent driver in the future.